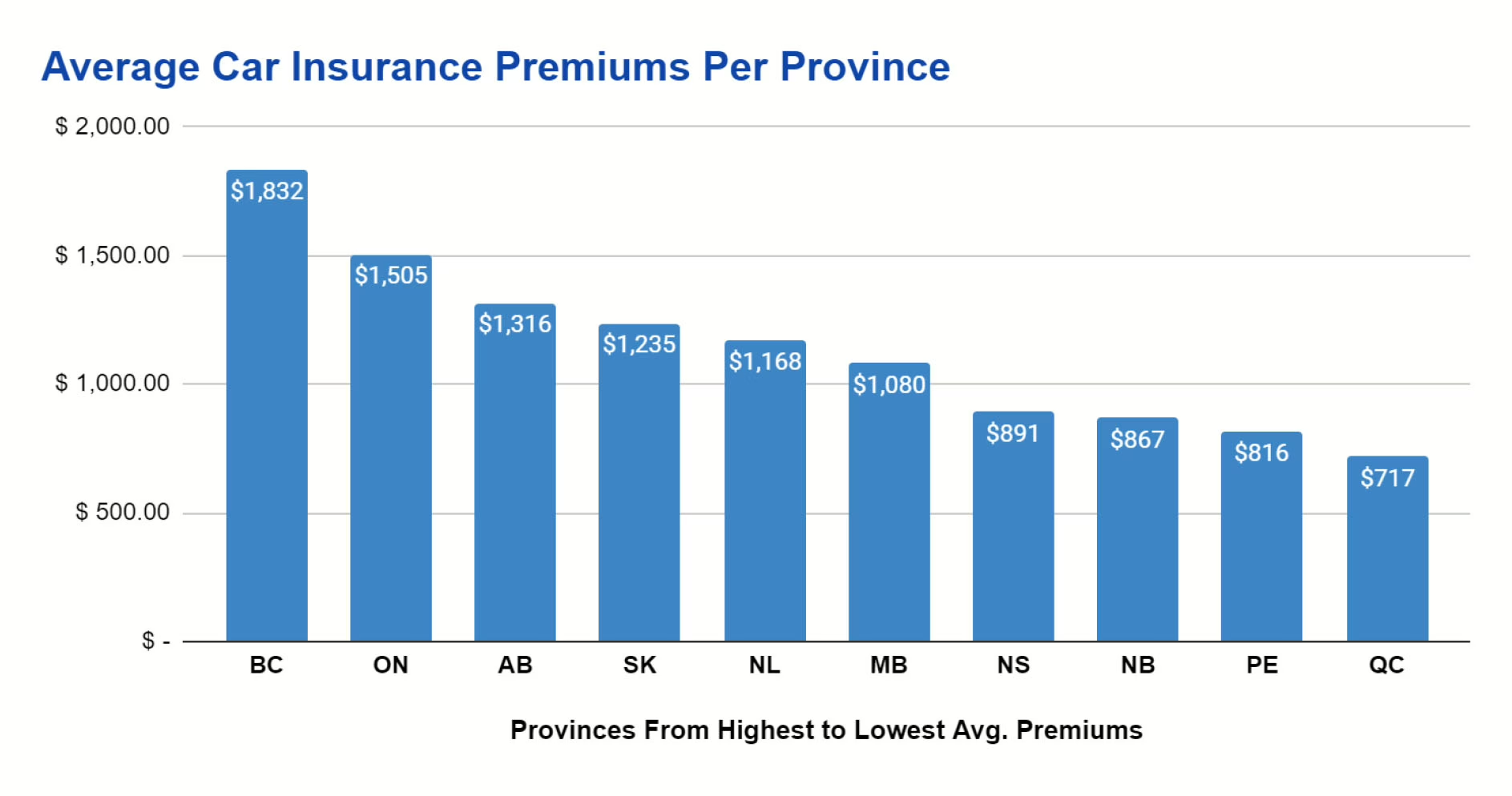

Car insurance costs can seem unpredictable, but they’re not. Insurers use specific factors to calculate how much you pay, and knowing these can save you money. Everything from your driving record to where you live affects your rate. By understanding the key influences, you’ll be better equipped to make informed choices and even reduce your costs.

Driver Characteristics

When it comes to determining your Car insurance costs, your personal characteristics play a significant role. Insurers assess several factors to gauge how risky you might be as a driver. Let’s break down how age, driving history, gender, and marital status can impact what you pay.

Age and Experience

Youthful energy comes with a price—especially when it comes to car insurance. Younger drivers, particularly those under 25, often face the highest premiums. Why? Insurance companies view them as high-risk due to limited driving experience and statistically higher accident rates. After all, practice makes perfect, and younger drivers are just starting to build their skills.

The good news is that Car insurance costs tend to stabilize as you get older and gain more experience behind the wheel. Drivers in their 30s, 40s, and 50s typically enjoy lower rates—assuming they maintain a clean record. But keep in mind that once you enter the senior category (around age 70), rates may creep up again due to concerns about slower reflexes and health matters. For more insights on how age influences premiums, you can refer to MarketWatch’s guide on car insurance rates by age.

Driving Record and Violations

A spotless driving record is like a golden ticket for low car insurance rates. Insurers look closely at your history on the road, and if you have a clean slate, you’re seen as a safer bet. This means fewer claims and, ultimately, lower Car insurance costs.

On the flip side, accidents, speeding tickets, or other violations can quickly surge your insurance costs. Why? Insurers need to account for the increased likelihood of future claims. Something as minor as a moving violation could result in a premium hike, while more serious incidents, like DUIs, can cause even greater increases. Want to know more about how your driving record affects your insurance? Check out this resource by Cathy Sink Agency.

Gender and Marital Status

Did you know that your gender and marital status can have a subtle influence on your insurance premiums? While some states have banned the use of gender in calculating premiums, in places where it’s allowed, male drivers—especially young males—often face higher rates than their female counterparts. This stems from statistical data showing that young men are more likely to engage in risky driving behaviors.

Marital status also plays a role. Married drivers generally pay lower premiums compared to those who are single, divorced, or widowed. Why? Insurers often deem married individuals as being more responsible and financially stable. This perceived reliability can translate into slightly lower risk on the road. You can learn more about this factor at The Zebra’s explanation of marital status and car insurance.

As you can see, these personal characteristics affect how insurers view risk, which ultimately shapes your premium. Understanding these factors can help you take steps to reduce your costs where possible.